Feeling stuck because a past repo is haunting your credit report? You’re not alone.

Many people find themselves in this tricky spot, wondering if they’ll ever drive a car they love again. The good news? There’s hope. Even with a repossession on your credit, getting a car loan isn’t just a dream—it’s achievable. Imagine cruising in your own car, feeling the freedom of the open road.

Sounds great, right? We’re here to guide you through the maze of financing options available to you, despite that pesky repo. Curious about how to turn this challenge into an opportunity? Keep reading to discover the strategies that can put you back in the driver’s seat and reclaim your financial independence.

Credit: www.instagram.com

Understanding Repossession Impact

Car loans with a repossession on credit can be challenging. A repo affects your credit score significantly, making new loans harder to obtain. Understanding the impact helps in planning future financial decisions wisely.

Understanding how repossession affects your credit score is crucial if you’re considering a car loan. When your vehicle is repossessed, it means that the lender has taken back the car due to missed payments. This can have a significant impact on your credit profile, which can linger for years. But what exactly happens to your credit when repossession occurs, and how can you navigate these challenging waters?What Is Repossession?

Repossession occurs when a lender takes back the car because you’ve failed to make payments. It’s a legal right they have, outlined in your loan agreement. This action is not only stressful but also has lasting effects on your financial health.How Does Repossession Affect Your Credit Score?

A repossession can drastically lower your credit score. It signals to lenders that you’re a risk, making it harder to get credit in the future. The repossession mark stays on your credit report for seven years, similar to other negative marks like missed payments.Understanding The Repossession Process

Lenders typically don’t repossess your car after a single missed payment. They might contact you to discuss the situation. However, ignoring these communications can lead to repossession. Once the car is taken, the lender may sell it to cover the loan balance.What Happens To The Remaining Balance?

If your car is sold for less than what you owe, you might still be liable for the remaining balance, known as a deficiency balance. This debt doesn’t disappear and can further affect your credit score if not managed.Can You Avoid Repossession?

Yes, there are ways to avoid repossession. Contact your lender at the first sign of trouble. They may offer solutions like a payment plan or loan modification. Open communication can be a key to finding a solution that works for both parties.How To Rebuild Your Credit After Repossession

Rebuilding credit after repossession takes time and commitment. Start by ensuring all other bills are paid on time. Consider secured credit cards or credit-builder loans to demonstrate responsible credit behavior. Over time, these efforts can help improve your score. Understanding the full impact of repossession can empower you to make informed decisions about your car loan and financial future. Have you experienced a repossession, or are you worried it might happen? Share your thoughts and let’s discuss practical solutions.Credit Report Implications

Understanding the implications of a car loan repossession on your credit report is crucial. A repossession can significantly impact your credit score, affecting future financial opportunities. Let’s delve into the details of how a repo can alter your credit landscape.

Impact On Credit Score

A repossession remains on your credit report for seven years. It can lower your credit score by 100 points or more. This drop can make obtaining new credit challenging.

Debt Collection And Your Credit Report

After repossession, the lender may sell the car. If the sale doesn’t cover the loan balance, you owe the remaining amount. This debt might go to collections. Collection accounts can appear on your credit report, further harming your score.

Potential For Lawsuits

If you fail to pay the remaining balance, the lender might sue. A court judgment can appear on your credit report. This negative mark can last for years, complicating your financial future.

Opportunities For Credit Repair

Despite these challenges, rebuilding your credit is possible. Paying existing debts on time helps. Consider working with a credit counselor to improve your financial health.

Options For Financing With Repossession

Facing repossession can be daunting, but financing options exist. Those with repossession history have choices to rebuild their financial path. Understanding these options can guide you in securing a car loan. Let’s explore financing avenues available for individuals with repossession.

Traditional Lenders

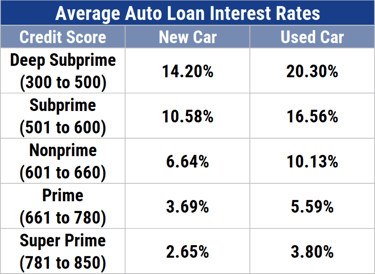

Traditional lenders might hesitate with credit histories showing repossession. Banks and major finance companies usually prefer borrowers with clean records. Their interest rates and terms are typically better for those without past credit issues.

Yet, some traditional lenders have programs for higher-risk borrowers. These programs may come with higher interest rates. It’s vital to check what each lender offers.

Subprime Lenders

Subprime lenders specialize in loans for borrowers with poor credit. They understand the challenges and offer tailored solutions. The interest rates can be higher, reflecting the risk they undertake.

These lenders often have flexible payment plans. It’s key to compare offers and choose the one that fits your budget. Subprime lenders provide a chance to improve credit scores over time.

Credit Unions

Credit unions are member-focused and might offer competitive rates. They often look beyond credit scores, considering the member’s overall financial situation. Membership benefits can include lower fees and personalized service.

They are known for their willingness to work with members facing credit challenges. Joining a credit union may provide access to more lenient loan terms. It’s worth exploring local credit unions for potential financing solutions.

Improving Credit Score

Facing a car loan with a repo on credit can feel overwhelming. Paying off outstanding debts helps improve your credit score. Timely payments and maintaining a low credit utilization are key steps.

Improving your credit score after a car loan with a repo can seem like a daunting task, but it’s entirely achievable with the right approach. It’s about making informed decisions and taking consistent steps toward financial health. With a focus on good habits, you can gradually lift your credit score and regain financial confidence.Timely Bill Payments

Consistently paying your bills on time is crucial. It shows lenders that you’re reliable and can manage your financial responsibilities. Consider setting up automatic payments to avoid missing due dates and incurring late fees. A personal reminder: when I started automating my utility bills, I noticed my credit score began to climb steadily. Have you considered what a late payment might be costing you in terms of credit score points?Debt Reduction Strategies

Reducing outstanding debt is another effective way to boost your credit score. Start by tackling high-interest debts first, as they can quickly spiral out of control. You might find the snowball method rewarding, where you pay off smaller debts first to build momentum. Breaking down your debts into manageable chunks can make the process less overwhelming. What small steps can you take today to start reducing your debt?Credit Monitoring Tools

Using credit monitoring tools can provide valuable insights into your credit health. They help you stay informed about changes in your credit report and can alert you to any suspicious activity. Some tools even offer tips tailored to your credit profile, making them a great resource in your credit improvement journey. Regular monitoring can also motivate you to maintain good credit habits. Have you explored any credit monitoring services that suit your needs?Negotiating With Lenders

Negotiating with lenders for a car loan can be challenging with a repossession on your credit. Clear communication and a solid plan can help improve your chances. Highlight steady income and recent financial improvements to reassure lenders of your repayment ability.

Negotiating with lenders after a car repossession on your credit can be a daunting task. However, approaching the situation strategically can turn the tide in your favor. Understanding how to effectively communicate your circumstances and improvements can significantly impact the outcome.Explaining Repossession Circumstances

Start by clearly detailing the events leading up to the repossession. Was it due to a temporary job loss or an unexpected medical bill? Lenders are more likely to understand if you explain your situation with honesty and clarity. Provide documentation that supports your story. This could be termination letters, hospital bills, or any other relevant paperwork. It’s crucial to show that the repossession was not a result of negligence but rather unavoidable circumstances. Consider sharing a personal story. For instance, explain how a sudden layoff impacted your financial stability but emphasize how you’ve managed to regain control. Personal anecdotes can humanize your situation, making lenders more empathetic to your case.Presenting Financial Improvements

Once you’ve explained the past, shift focus to your current financial status. Highlight any positive changes such as a new job, increased income, or reduced expenses. Lenders need assurance that you’re now in a better position to manage debt. Prepare a budget to demonstrate your commitment to financial responsibility. This could include a detailed plan showing how you will meet future obligations. Providing a clear, structured budget can instill confidence in lenders regarding your ability to repay the loan. Share specific examples of improved credit behavior. Have you been making on-time payments on other debts? Highlight these efforts as evidence of your renewed financial discipline. Showing proactive steps towards improvement can significantly enhance your negotiating position. Engaging with lenders from a place of transparency and preparedness can open doors to better terms and conditions. Are you ready to take control of the narrative and turn a repossession mark into a stepping stone for financial growth?

Credit: www.badcredit.org

Alternative Transportation Solutions

Finding a car loan with a repo on credit can be challenging. Lenders often view repossession as a risk, but some offer solutions for borrowers with past credit issues. Exploring various lenders and credit unions might help secure a loan despite previous repossessions.

Alternative transportation solutions can be a lifeline after a car loan repossession. Losing access to a vehicle can disrupt daily life significantly. Exploring different ways to commute ensures mobility and flexibility. There are various options that can cater to different needs and budgets.Car Sharing Programs

Car sharing programs offer a practical way to access a car without ownership. They provide vehicles on demand for short periods. Joining these programs can be cost-effective. Members pay only for the time and distance driven. This option eliminates maintenance worries. It also reduces the financial burden of car ownership.Lease Options

Leasing a car can be a viable alternative. It allows access to a newer vehicle with manageable monthly payments. Lease agreements often include maintenance and repair services. This ensures the vehicle remains in good condition. Leasing can provide a reliable mode of transportation without long-term commitment.Public Transport Benefits

Public transport offers a reliable, budget-friendly solution. It connects to most urban and suburban areas effectively. Using buses, trains, or trams reduces travel costs. It can also minimize environmental impact. Public transport networks are well-developed in many cities. They provide frequent and convenient service, making daily commuting stress-free.Legal Rights And Protections

Understanding your legal rights and protections is crucial if a car loan results in repossession on your credit report. These rights can shield you from unfair practices and help you navigate the complex world of credit and repossession. Knowing these protections can make a significant difference in managing your financial situation.

Fair Credit Reporting Act

The Fair Credit Reporting Act (FCRA) ensures accuracy in your credit report. It gives you the right to dispute errors. If repossession details are wrong, you can challenge them. This act also requires creditors to inform you of negative information being reported. This transparency helps you stay informed about your credit profile.

State-specific Laws

Each state has unique laws governing car repossession. Some states require notification before repossession, while others allow immediate action. Understanding your state’s laws can prevent unexpected repossession. Certain states offer a redemption period, allowing you to reclaim your car by paying off the debt. Knowing these laws can empower you to protect your rights effectively.

Seeking Professional Financial Advice

When dealing with a car loan with a repo on your credit, seeking professional financial advice is vital. Professional guidance can provide clarity and direction. Experts can help you understand your financial situation better. They can offer tailored solutions to improve your credit standing.

Credit Counseling Services

Credit counseling services offer valuable assistance in managing debt. They provide a comprehensive review of your financial situation. Counselors work with you to create a budget plan. This plan aims to help you make timely payments. They also negotiate with creditors to lower interest rates or fees.

These services can offer educational resources. Learning about financial management is crucial. It empowers you to make informed decisions. With better knowledge, you can avoid future financial pitfalls.

Financial Planning Assistance

Financial planning assistance helps you set financial goals. Planners assess your current financial status. They help you develop a realistic strategy to achieve your goals. This includes saving for emergencies or retirement.

Planners also guide you in investment choices. They can advise on which investments suit your financial goals. Such guidance ensures you make decisions that align with your financial future.

With a financial planner, you gain insights into managing your finances effectively. This support can be crucial in improving your credit score. It also helps in rebuilding financial stability after a repossession.

Credit: www.cardrates.com

Frequently Asked Questions

Can I Still Get A Loan With A Repossession On My Credit?

Yes, you can still get a loan with a repossession on your credit. Lenders consider factors like income, credit score, and financial stability. Improve your credit and demonstrate responsible financial behavior to increase approval chances. Some lenders specialize in working with individuals with past credit issues.

Can You Get A Car Loan With A Repo And Bad Credit?

Yes, you can get a car loan with a repo and bad credit. Explore lenders specializing in bad credit loans. Improve approval chances by offering a larger down payment or adding a co-signer. Maintain a stable income and address credit issues for better terms.

Can I Buy A Car With A Repo On My Record?

Yes, you can buy a car with a repossession on your record. Improve your credit score first. Consider higher interest rates or larger down payments. Explore options like subprime lenders or buy-here-pay-here dealerships. Maintaining consistent payments can help rebuild your credit.

How Long After Repo Can You Finance A Car?

You can finance a car immediately after a repo, but expect higher interest rates. Improve credit by paying off debts and building a positive payment history. Lenders prefer a credit score above 600 for better terms. Shop around to find lenders who specialize in bad credit auto loans.

Conclusion

Navigating a car loan with a repo on credit is possible. Start by understanding your credit report. Fix errors quickly. Shop around for lenders who specialize in bad credit. Compare rates and terms carefully. A larger down payment can help your chances.

Improving your credit score over time boosts your approval odds. Stay realistic about your budget and loan terms. Being informed and proactive makes the process smoother. Remember, patience and persistence are key. Good luck on your car loan journey!